Looking at the markets one could get a feeling the global economy is improving. An early estimate of current private-sector business activity, however, signals a sharp slowdown in both developed and emerging countries. This is mainly due to a surge in the cost of living and the persistence of inflation pressures.

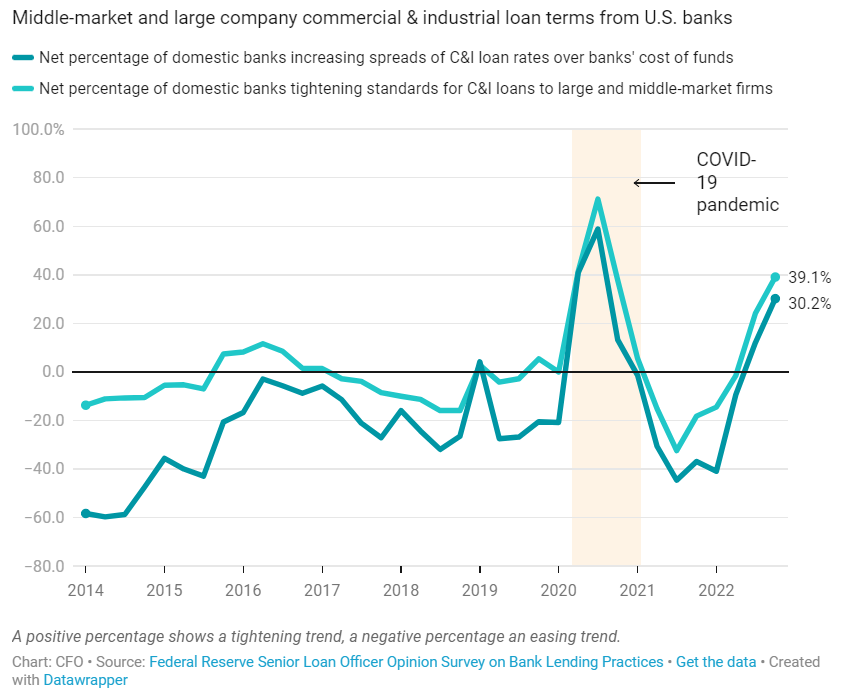

The corporate sector responded to the cloudy outlook by cutting costs and optimizing risk controls. Commercial banks in the US, for example, have opted for tightening lending terms for medium-sized and large businesses and commercial real estate. Credit-card and other consumer loan contracts have also been renegotiated.

The bottom line is that corporates will face higher funding costs, making it harder for the issuer to refinance its debt. In this context, Standard & Poor’s analysts forecast a spike in the default rate of speculative-grade issuers through next September. S&P projects the trailing 12-month default rate will reach 3.75% by then.

Fitch Ratings economists expect bond defaults to pick up by the end of this year due to some upcoming distressed debt exchanges (DDEs). “In DDEs, generally, holders of some of a company’s debt take a haircut on their principal amount. In exchange, they move up in payment priority in the form of secured debt. DDEs are technically defaults.”

If that’s not worrying enough, total household debt jumped by US$351 billion for the July-to-September period to a record $16.5 trillion. To protect itself from financing squeeze, the banking industry set aside $13.05 billion for credit risk in the third quarter, up from positive provisions of $10.95 billion a quarter earlier. Overall, financial institutions increased their provisions for losses on problem loans for the sixth consecutive quarter.

What are the chances the worst-case scenario becomes reality? The answer depends on the future economic situation. A Deutsche Bank Securities analyst predicts a recession in the third quarter of 2023, which will lead to a jump in the unemployment rate to 5.6%. The good news is that the tightening of lending standards by banks makes it easier for the US Federal Reserve – the regulator may not have to raise the rate above 5%.

As for Asia, investors should keep an eye on the epidemiological situation in the Middle Kingdom. China’s soaring Covid cases could end up in new shutdowns.

Talking about perspectives, Wall Street analysts believe in a “reset” of the Chinese market next year. How it will actually turn out no one knows. To reduce exposure to various drivers of systematic risk it would be recommended to rely predominantly on stocks with high dividend yields. This will allow investors not only to survive the new roller coaster but also profit from it.