China has been inundated by foreign currency, as its trade surplus has surged to a record $600 billion-plus per month during 2021.

China’s export performance creates a massive imbalance of supply and demand for its currency. Chinese exporters are selling excess dollars to buy yuan, and the People’s Bank of China appears to be buying dollars on the open market to slow the appreciation of the Chinese currency.

In the Chart of the Day, we see that surges in dollar deposits at Chinese banks coincided with bursts of yuan appreciation in the past.

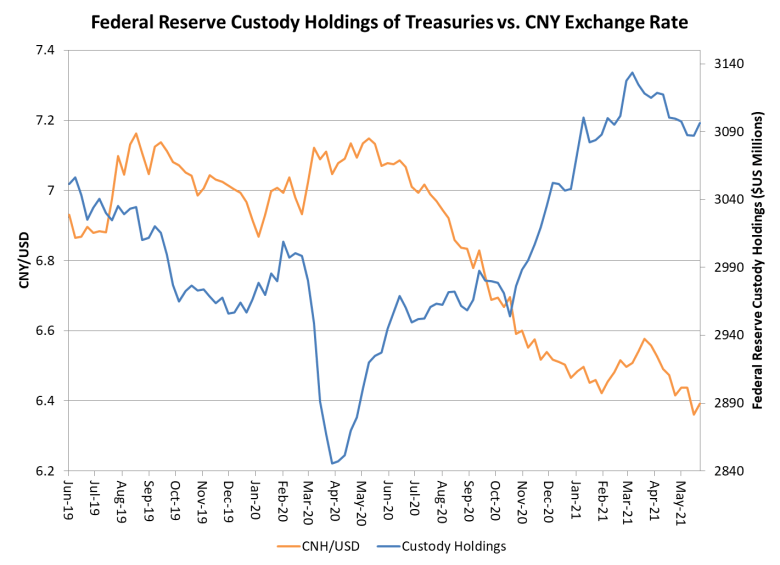

China’s foreign exchange reserves have risen by about $120 billion since the beginning of 2020. The People’s Bank of China appears to have bought US Treasury securities with the proceeds. Federal Reserve holdings of Treasury securities in custody for foreign central banks rose by about the same amount as China’s reported reserves.

In the above chart, we see that China’s currency appreciated as Fed custody holdings increased. The People’s Bank of China has probably intervened in the foreign exchange markets, buying dollars on the open market, to prevent the yuan from appreciating too quickly – and buying Treasury securities with the dollars it purchased.

The yuan has appreciated against the US dollar by 11 percent over the past year, and the Chinese authorities want to slow the currency’s rise, if not stop it. A rising currency helps buffer the Chinese economy against imported inflation, a pressing concern after May’s near-record 9% year-on-year jump in the producer price index. But a disorderly rise in the yuan could be disruptive.

For the time being, China’s authorities are trying to hold back yuan appreciation. But they are fighting against a floodtide of dollars pouring into China, and the likeliest outcome is continuing gains for the yuan, perhaps to 6.15 by the end of this year.