There are two types of viruses: computer and biological ones. Neither of them brings happiness to those who have been affected. However, they do leave important marks, and in some cases, the negative effects can last years or even trigger new issues.

For example, the Covid-19 pandemic has not only caused health issues but also led to a new financial crisis. It might have been seen as one the shortest for financial markets, but we shouldn’t be so naive.

First, indices’ recovery was a result not so much of a good epidemiological situation, but monetary instruments implemented by the world’s most influential central banks. The only problem is that they also have their own price. Here we need to ask the first question: Who will pay for the Covid crisis bailout?

The answer is very simple – we will. Despite the fact that markets are near record highs, there are still millions of people who haven’t been able to recover their jobs. Thousands of companies were closed and many probably will never open again.

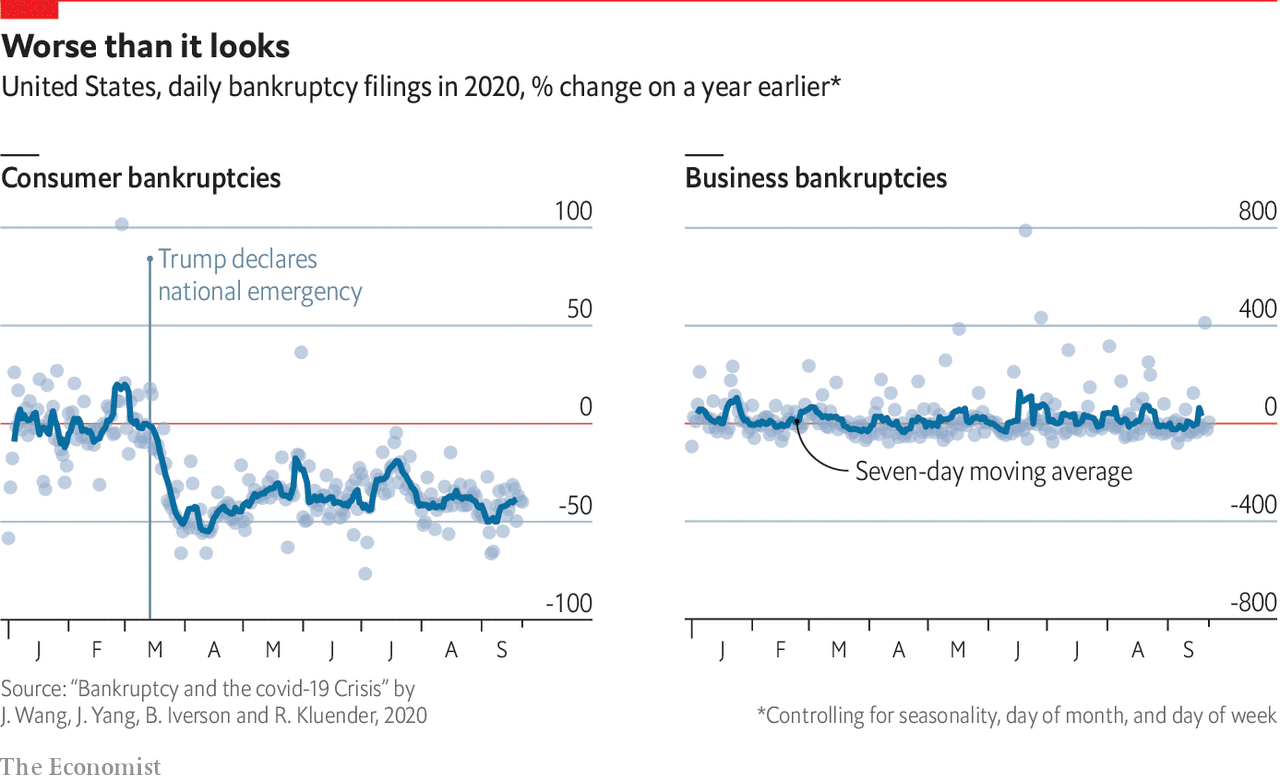

Based on a 9.2% unemployment rate in the US in the fourth quarter of 2020, researchers initially predicted that bankruptcies would finish the year with a 140% increase YoY.

Bankruptcy filings slowing?

It is also important to mention that a US company filing for bankruptcy doesn’t necessarily mean it will disappear. Instead, bigger companies usually do this to restructure and settle on new repayment terms for their debts so they can remain open. Unfortunately, small and medium-sized enterprises can’t normally afford such an option.

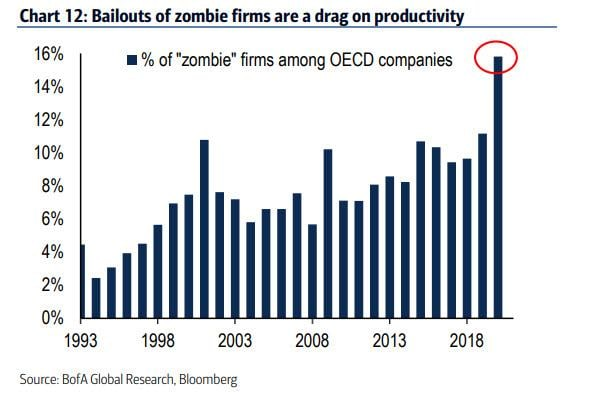

For now, it may look like US bankruptcy filings have slowed but once again, we shouldn’t be naive, the bang is yet to come. Many of the companies that should have closed down have simply been reincarnated into zombie firms.

They are neither dead nor alive. The amount of debt on their balance sheets is so high that any cash generated is being used to pay off the interest. Thus the company can’t grow as it doesn’t have spare funds to invest. This, in turn, means it can’t employ more people.

To be fair, this problem is not new, it has been with us for years, and the reason is cheap loans due to low interest rates.

Zombie companies

Many zombie companies survive by issuing new debt that will allow the funding of operating losses and interest payments. If you ask which sectors are on the radar, unfortunately, there won’t be a clear answer. Basically, every sector is at risk, from entertainment to retail and beverages. The situation is only getting worse with additional lockdowns.

It is also true that some companies do benefit from the situation, especially IT businesses, but even they could eventually suffer if the global economy enters a new crisis.

Who else borrowed during the pandemic?

But companies are not the only ones that have fallen into debt distress. According to the International Monetary Fund, emerging-market governments issued US$124 billion in hard-currency debt during the first six months of 2020, with two-thirds of the borrowing coming in the second quarter.

The US public debt, on the other hand, hit a peak not reached since World War II. The UK government borrowed a net £36.1 billion ($47.1 billion) in September, pushing the total for the first six months of the year to £208.5 billion. That’s the highest figure since records began in 1993.

The increase in the average debt ratio in the euro area is estimated to be more than 15%, bringing it over 100%. It will climb by about 20% in France and about 30% in Italy and Spain.

What are the solutions?

Governments will have to find ways to repay these debts, something that won’t be easily achieved. One option could be to impose monumental tax increases. And who will bear the burden? As always, it will be the middle class, just like US tariffs on Chinese products were paid by American consumers.

In the end, these debts will cause future deficits and will sap the financial strength almost of every economy. Even the US might have to face paying much more in interest than previously forecast. Thus this money won’t go to hiring teachers or paying for hospital stays for the elderly.

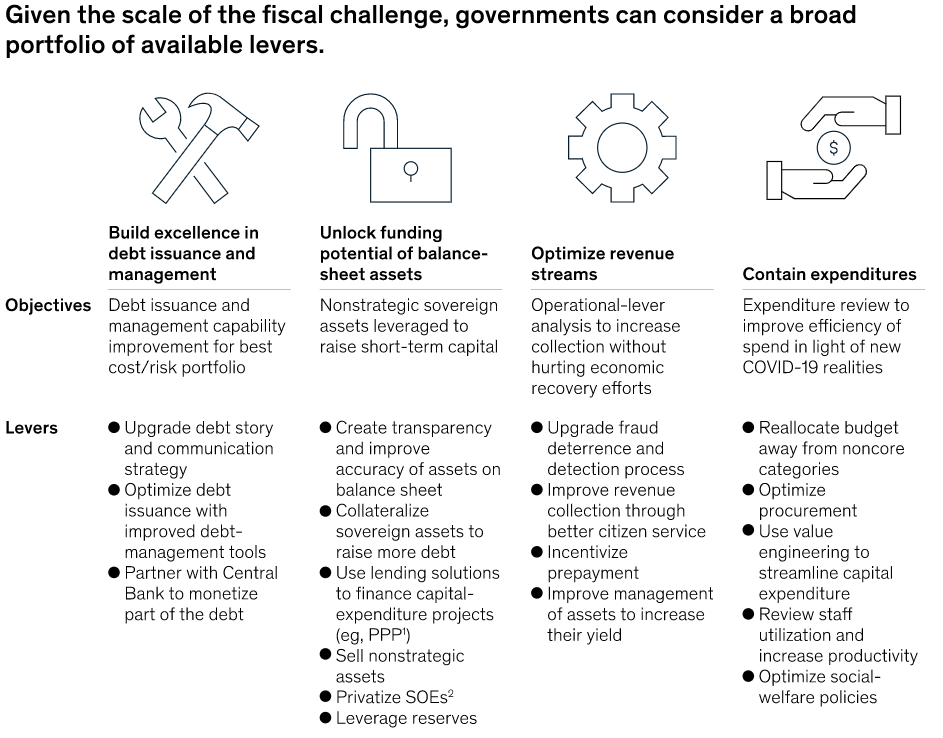

McKinsey researchers also suggest that governments will have to optimize revenue streams and contain some public spending. They also believe that using only tax increases to fund the deficit would raise taxation by 50%, which would hurt taxpayers, limit corporate investment, and reduce national competitiveness.

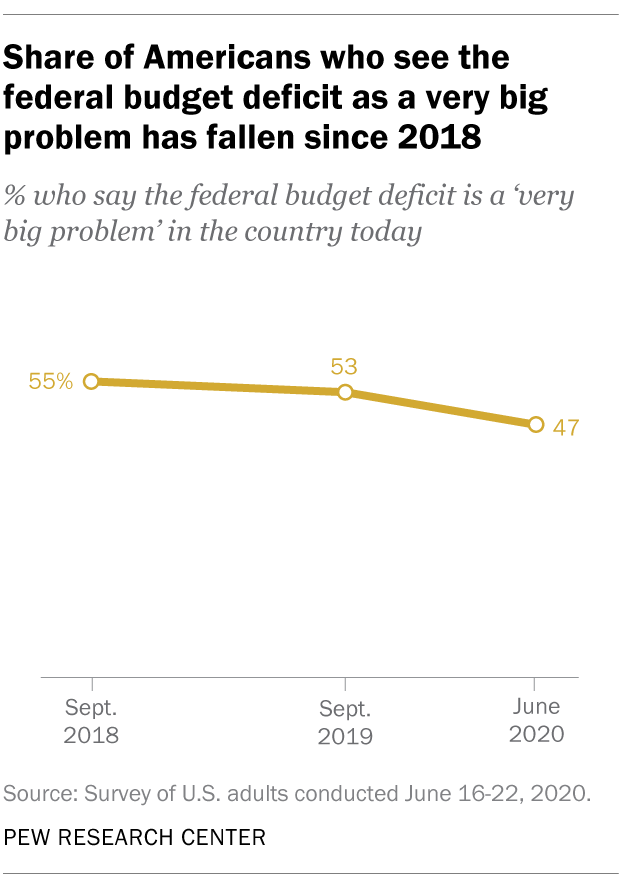

The crazy thing is that Americans appear not to be much more concerned about the deficit than they have been in recent years. The study suggests that just under half of American adults (47%) called the deficit “a very big problem,” down from 55% in the autumn of 2018.

In conclusion, it is clear that efforts taken so far to resolve the current problems have just postponed the ultimate consequences until some time in the future. If countries continue to increase their debt levels, they could have trouble raising cash at affordable rates. Other consequences could be depressed economic output and increased risk of a fiscal crisis.

Having said that, despite the fact that markets are overly positive, the situation is far from being the best, and the real consequences might be yet to come.