For a long time real estate has been considered one of the best long-term investments to protect against inflation. Unlike many other traditional investment products, real estate is not tied to the stock market, making it an efficient instrument to reduce risk and increase long-term returns.

Nevertheless, no asset class comes with a guarantee, and losses can be expected even for fixed-income investments. The negative impact of the Covid-19 outbreak on the labor market, the retail sector, and consumer demand is hurting the property market.

One of the advantages of real estate is appreciation. In 1940, the median home value in the US was just $2,938. In 1980, it was $47,200, and by 2000, it had risen to $119,600. In the UK, the price of an average house went from around £51,800 in today’s terms back in 1952 to around £211,400 ($274,900) in 2017.

On the other hand, by renting an apartment, smart investors can cover a major part of monthly expenses, including mortgage, interest, taxes, and insurance. Those people who can’t afford to buy a house could invest in real estate investment trusts (REITs), companies that own and collect rent from commercial and residential properties.

However, real-estate values are also subject to fluctuations, as happened in 2008 and is being repeated now. Real house prices react differently to economic shocks, depending on such factors as the growth rates of the underlying population and real income in the area, the size of the area, and construction costs.

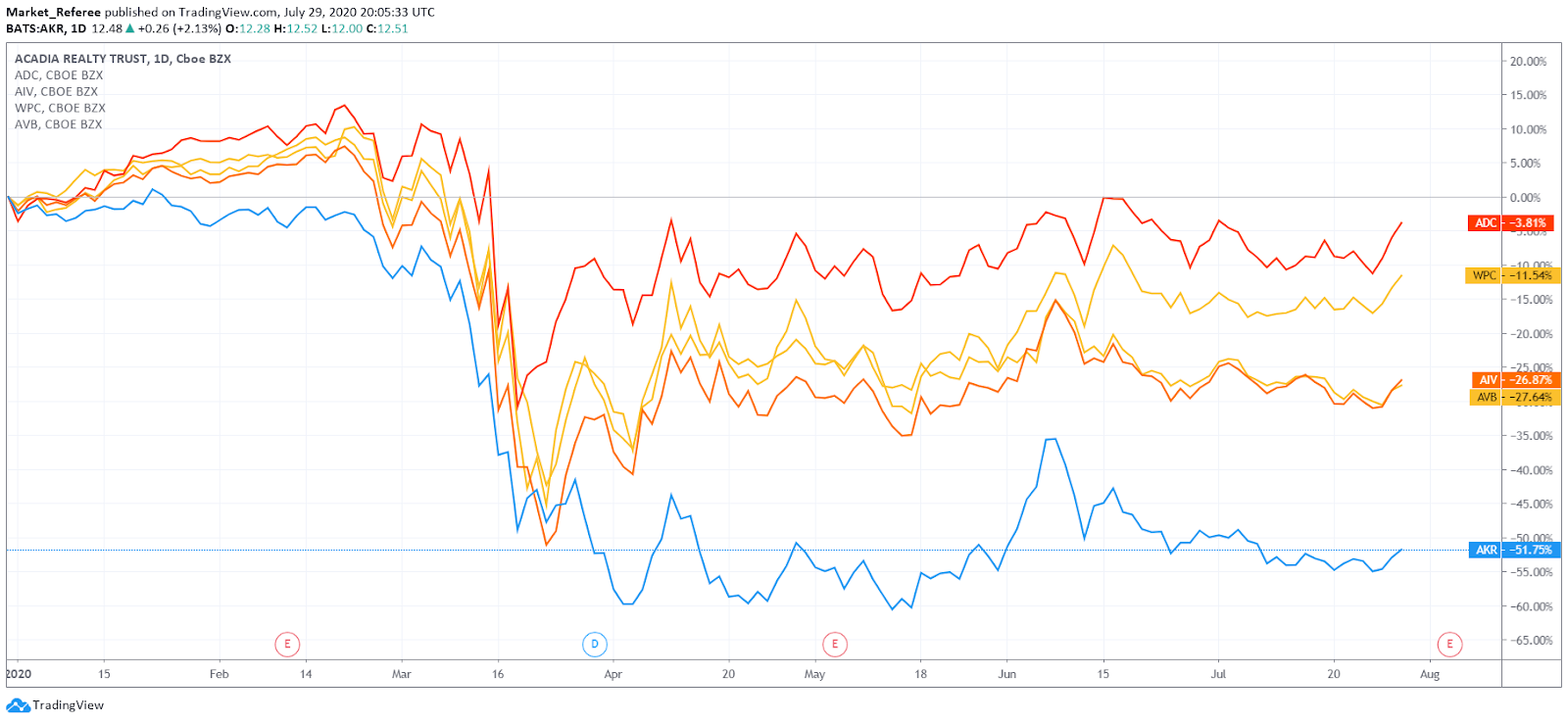

Currently, the housing market is going through a turbulent phase. As we can see on the following graph, the vast majority of REITs have suffered a broad selloff amid the coronavirus pandemic. According to Fitch ratings, US Mall REITs’ Cash Flow risk increased amid lower near-term rent collections. For that reason, before investing in REITs, it is crucial to understand both their business models and risks.

The impact of Covid-19

The economy is more complicated than just stocks and indices. Despite the fact that the US Federal Reserve injected trillions of dollars to prop up the economy through a series of unprecedented emergency initiatives, including the purchase of junk bonds, the situation is still very serious.

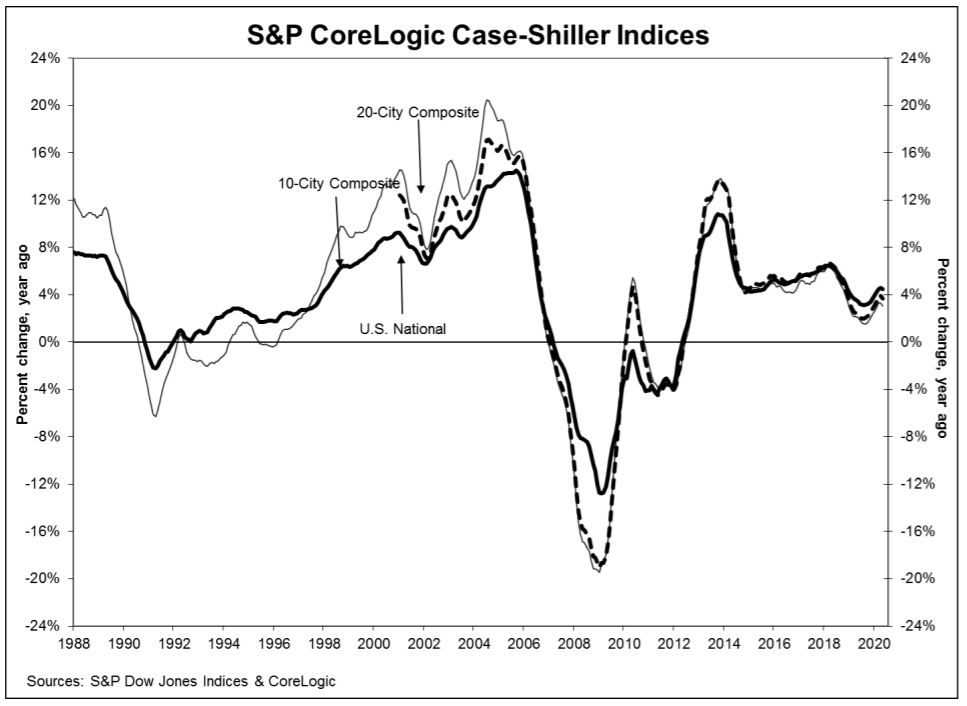

According to the latest results for the S&P CoreLogic Case-Shiller Indices, the growth of US home prices began slowing down in May, as home sales fell for a third month due to unprecedented quarantine measures that caused a shutdown of economic activity in many cities.

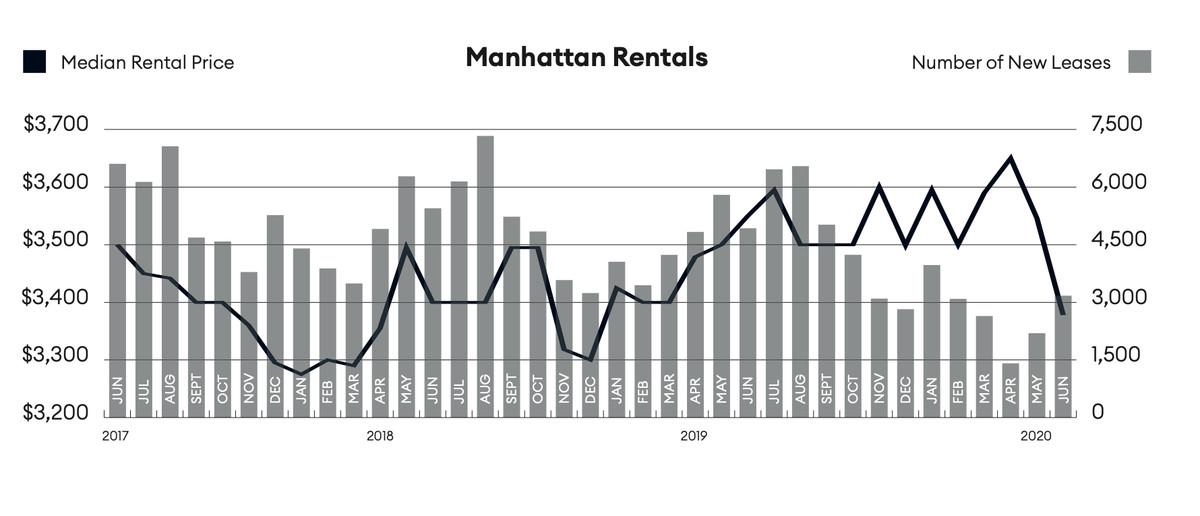

Average home prices in major metropolitan areas across the US grew 4.5% in May, down from 4.6% the previous month. The number of closed sales in the second quarter in the case of the Manhattan real-estate market, for example, fell 54% year on year. The median sale price fell 17.7%, compared with the same time last year, to $1 million.

More important, thousands of people are leaving New York, causing a drop in rents for the first time in years and the decline is expected to continue through the rest of 2020. Overall, the Manhattan vacancy rate grew to 3.67%, a 14-year high.

It is also important to consider that the quarantine forced many to move back in with their families, and it is not clear how many students will return, with universities shifting many classes online.

Even though Fitch’s 2020 high-yield default rate forecast for real estate is 3%, compared with the overall 5%-6% expectations, in 2009 this number was around 12%.

Government and business response

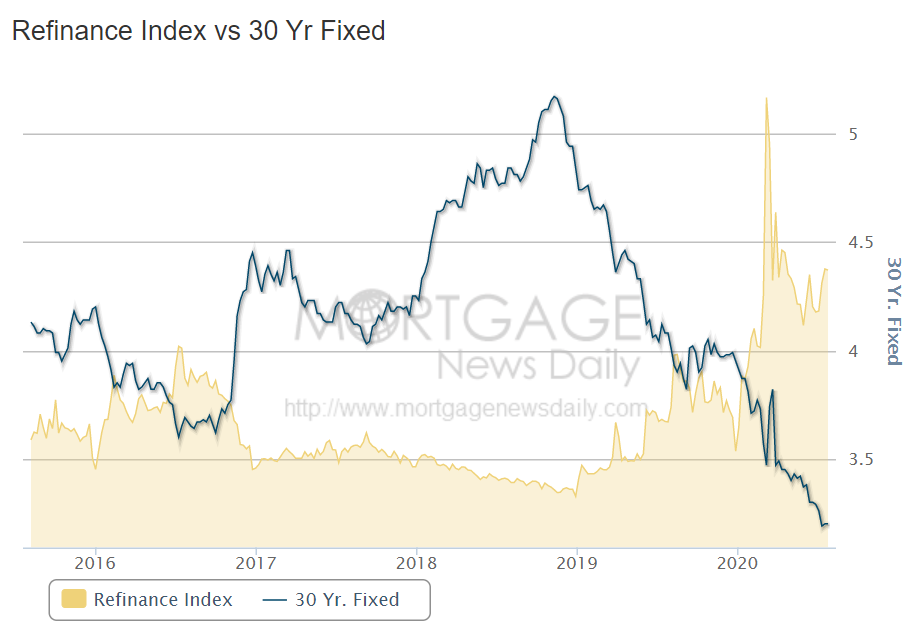

With a growing demand to refinance home loans, Wells Fargo increased the requirement for new clients to bring at least $1 million in balances if they want to refinance a jumbo mortgage, up from a previous level of $250,000.

On the government level, the Federal Reserve launched a $1.25 trillion program to purchase agency mortgage-backed securities in order to provide support to mortgage lending and housing markets and to foster improved conditions in financial markets more generally.

Housing market forecast

Fitch Ratings came to the conclusion that Spain will suffer the most significant fall in house prices, decreasing by 8-12% in full-year 2020. Australian prices will lose around 5-10%, whereas the UK will experience a downfall of 3-7%.

Lower wages and confidence, as well as lower expected population growth, are expected to affect demand for new housing in Australia. Thus it shouldn’t be a surprise that the demand for both new and established housing has fallen.

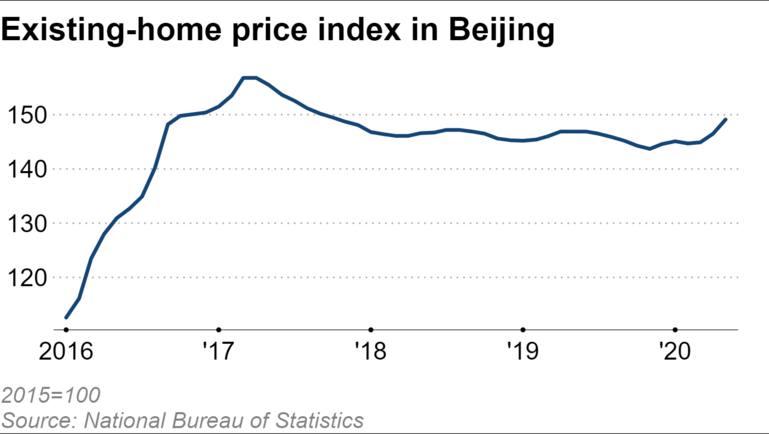

China’s property bubble

For the past few years, we have been observing a growing housing bubble in China. Apparently, it is already eclipsing the one we saw in the US in the 2000s. According to The Wall Street Journal, house prices keep rising higher and investors are looking for deals despite millions of job losses and other economic problems.

It is also worth mentioning that the Chinese government apparently doesn’t want to let the market fall, giving an incentive to keep buying houses.

However, we shouldn’t forget that China’s population is more than four times that of the United States.

Goldman Sachs found that the total value of Chinese homes and developers’ inventory hit $52 trillion in 2019, thus twice the size of the US residential market. The situation could worsen if China’s currency depreciates, pushing even more people to buy housing to protect their funds.

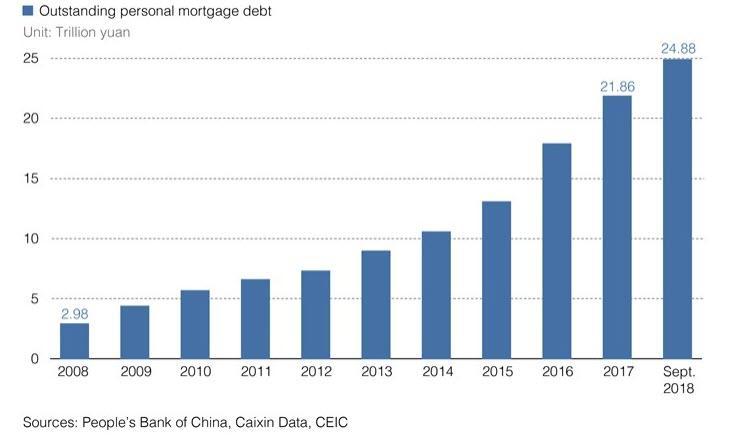

However, eventually even this bubble will burst. The question is when. Meanwhile, the situation is only getting worse, with mortgage debt exploding.

In conclusion, the second half of the year is going to be the real test for the property market, as government stimulus programs come to an end. The real problems will come with a rise in interest rates. We also should not forget that in the US more than 20% of the nearly 110 million renters are at risk of eviction, as moratoriums on rent payments due to Covid-19 restrictions begin to end.