Forced quarantine has bankrupted of hundreds of companies, and millions of people have lost their jobs. In terms of mental health, there has been a substantial increase in stress and anxiety. Loneliness, depression, harmful alcohol consumption, drug use and self-harm or suicidal behavior are also expected to rise.

Border restrictions are slowly being eased around the world and people can finally leave their homes without the fear of being fined, but quarantine measures could be reimposed.

Croatia has already reimposed quarantine for visitors from its four Balkan neighbors, according to Euronews. The British Broadcasting Corporation reported that German authorities in the state of North Rhine-Westphalia have reimposed lockdowns. China locked down 40 neighborhoods of Beijing after a cluster of cases in June.

Nevertheless, this doesn’t mean that all industries will be equally affected. Some may benefit from a second lockdown as they did in the second quarter. Among them were data-storage services, online food ordering and delivery platforms, hardware and building supplies retailing, and e-commerce.

For a comparison of productivity changes, see this chart:

There is one more segment that has experienced substantial growth during the Covid-19 crisis – the sustainable finance market. Companies in all sectors, from energy to materials to technology and beyond, have engaged in finance activities aimed at environmental, social or governance (ESG) benefits.

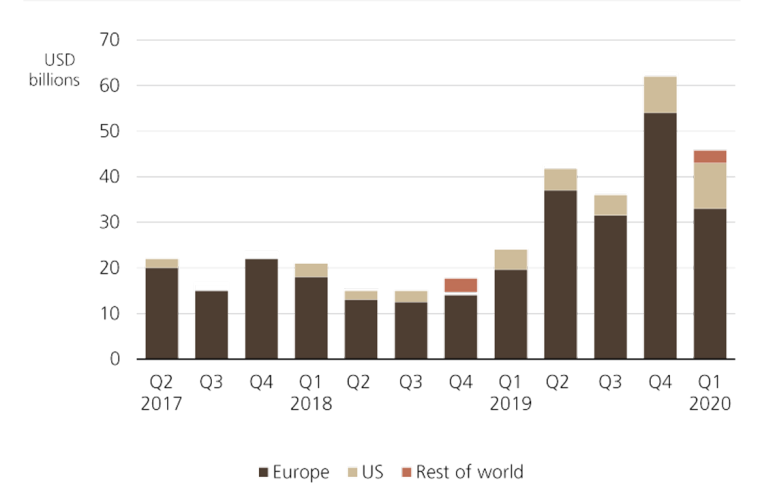

Quarterly sustainable fund flows

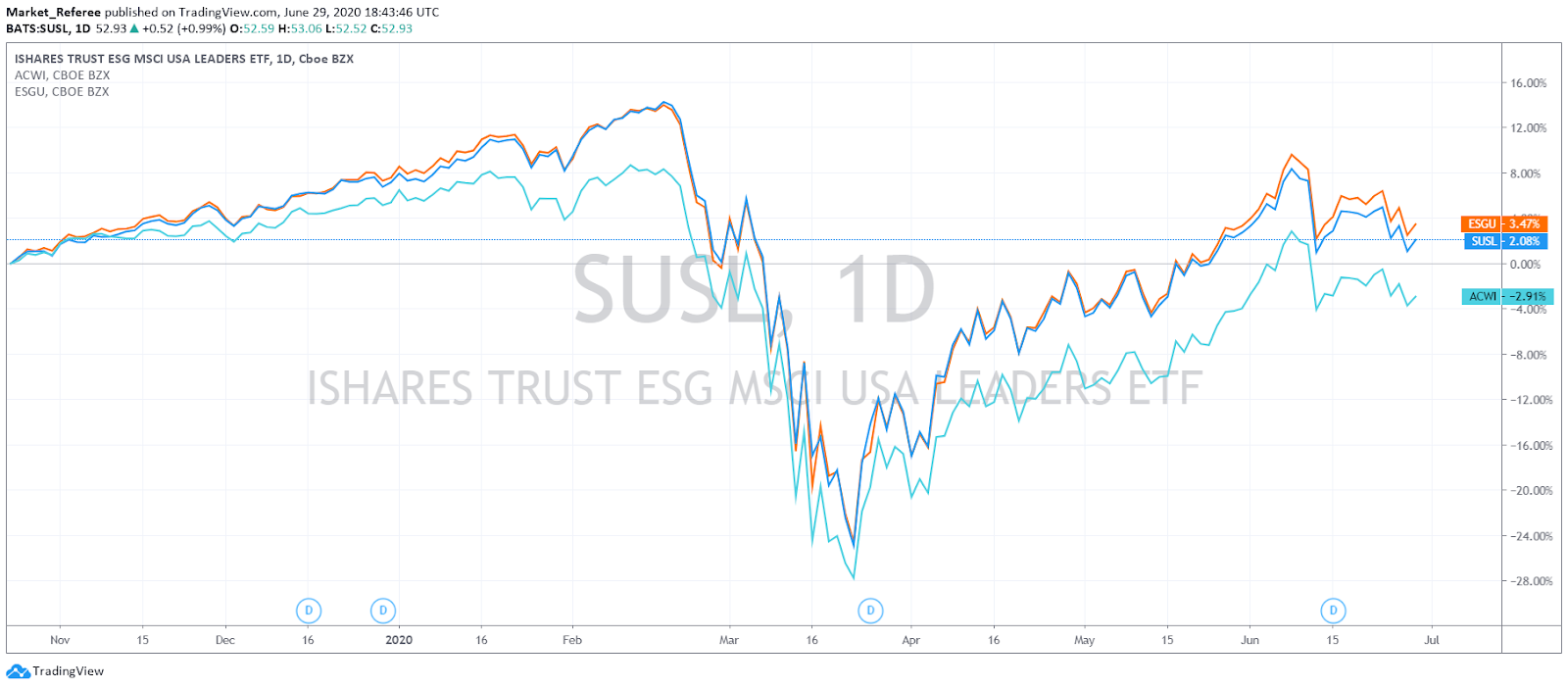

Theoretically, because of the Covid-19 disruption, companies could have refused to fulfill sustainability commitments and related decarbonization activities. Nevertheless, companies continued to push sustainability activities despite the pandemic. In addition, three major MSCI ESG funds outperformed non-ESG equivalents in May 2020.

According to UBS, the MSCI Asia ex-Japan ESG Leaders index also outperformed the regional MSCI Asia ex-Japan benchmark by more than 200 basis points year-to-date. It is possible that better performance of Asia ex-Japan ESG leader strategies can be contributed to the exclusion of gaming, alcohol, and fossil fuel stocks from the index. Thus, a priori we could say that ESG leaders represent a safer investment option.

In five years, the sustainable market classification changed from niche to mainstream. In 2019, the sustainable debt market raised over $450 billion in new bonds and loans for ESG purposes. The cumulative sustainable debt market that year surpassed $1 trillion issued since creation.

It is worth mentioning that in June, Copenhagen Infrastructure Partners raised $1.7 billion for a bet on renewables infrastructure, whereas venture capital firms Prime Coalition and Pale Blue Dot each raised more than $50 million for early-stage climate tech. Thus we could say that slowly but steadily green investment is attracting more attention.

Nevertheless, we are observing a decrease in the companies’ investments into emission reduction to indirectly offset their own emissions. More than 665,000 voluntary carbon offsets were retired this May, according to the American Carbon Registry and Climate Action Reserve, down from 677,000 in May 2019 and 887,000 in May 2018. However, it is good that companies continued to offset retirement activity, pursuing decarbonization targets despite the pandemic.

Besides that, to meet the 2030 climate and environmental targets, around €470 billion (US$527 billion) in additional annual investments are needed. As announced, the European Green Deal Investment Plan aims to mobilize at least €1 trillion in public and private funds to achieve climate neutrality by 2050.

According to the European Capital Markets Institute, the problem now is that some companies cannot justify green investments yet. Inflows into climate-related investment funds could play a greater role in targeting solutions that are not yet competitive.

Climate stewardship by asset managers should be oriented toward clear outcomes. Institutional investors with a long-term outlook, insurance companies and pension funds for example, could use their track record when delegating external mandates.

This brings us to the conclusion that socially responsible investing (SRI) is becoming a new reality. Surging capital flow into the sustainable debt market has been also driven by growing investor demand for the securities. To stimulate investment opportunities, some markets began offering financial benefits for issuers structuring sustainable debt.

Overall, economic benefits and risks should attract investors’ attention to environment-related opportunities. As demand for sustainable investing grows, all companies are feeling the pressure to be more socially and operationally responsible. Thus there is no doubt that ESG investments will continue growing as the world becomes more aware of threats to the environment and the need for energy efficiency.