Capitalism is a system under which you can sell practically everything you see, from fresh air to smoke.

Back in 2016, British entrepreneur Leo De Watts made thousands of dollars selling bottles of British country air to Chinese buyers for £80 (US$106). At first sight, it may seem that this is a rich man’s whim, but it’s not that simple.

Despite all of China’s efforts, the country still suffers from some of the worst air quality in the world. High levels of smog lead to a wide range of diseases, such as chronic obstructive pulmonary disorder, heart disease, stroke, and lung cancer. According to the latest research, air pollution has caused around 49,000 deaths and $23 billion in economic losses in the cities of Beijing and Shanghai alone since January 1, 2020.

With the Covid-19 lockdown, air-pollution levels have generally fallen as coal-fired power plants and industrial facilities have been closed. Levels of nitrogen dioxide, a pollutant primarily from burning fossil fuels, were down as much as 30%, according to NASA.

As pandemic restrictions begin to lift, carbon-dioxide emissions have rebounded. In this context, it shouldn’t be a surprise if people use air purifiers and purchase bottles of fresh air.

The question then arises, why not increase fines for industries violating state air-pollution rules and make the usage of fossil fuels more expensive, thus providing an incentive to use them more efficiently?

Putting a price on emissions can lead to higher costs that put domestic industrial producers at a competitive disadvantage and may shift pollution abroad. Thus a balance should be found.

To control greenhouse gas (GHG) emissions, a total of 192 countries have signed and ratified the Kyoto Protocol, a 1997 treaty to stabilize the concentration of the GHGs in the atmosphere and thereby slow the increase in global warming.

In addition, European countries have developed an emission trading system (ETS) that allows companies to receive or buy emission allowances. By the end of 2019, systems worldwide had raised more than $78 billion cumulatively since 2009. In the case of the European Union, total revenue of €50.54 billion (US$58.97 billion) has been collected since the beginning of the program, €14.64 billion in 2019 alone.

After each year a company must surrender enough allowances to cover all its emissions, otherwise heavy fines are imposed. If a company reduces its emissions, it can keep the spare allowances to cover its future needs or else sell them to another company that is short of allowances. Thus polluters who would find it costly to reduce their emissions are allowed to buy emission allowances from polluters that can reduce emissions at lower costs.

In other words, the right to emit a particular amount of CO2 became a tradable commodity, just like stocks, bonds, or exchange-traded funds (ETFs).

You now can buy and sell carbon emission allowances on the spot and/or on a forward basis; buy EU Allowances (EUAs) or EU Aviation Allowances (EUAAs) on primary auctions; swap trades (EUAs/EUAAs/CERs); exchange settled carbon transactions; and even purchase primary certified reduction units (CERs) from project owners.

Carbon trading works like an energy commodities market, based mainly on future contracts.

There are two main types of trading systems: cap-and-trade and baseline-and-credit systems. In a cap-and-trade system, an upper limit on emissions is fixed, and emission permits are either auctioned out or distributed for free according to specific criteria (In 2020, the number of free emission allowances that may be handed out to power plants has to be 0%).

Under a baseline-and-credit system, there is no fixed limit on emissions, but polluters that reduce their emissions more than they otherwise are obliged to can earn “credits” that they sell to others who need them in order to comply with regulations they are subject to.

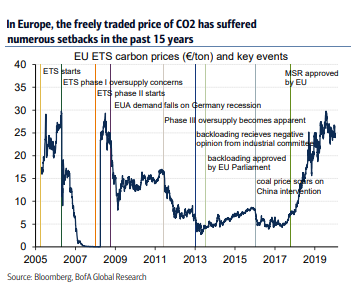

Normally, if the cumulative supply of allowances is too high, allowance prices will fall too low. And that’s exactly what happened during the global lockdown – allowances dropped from around €25 to around €15.

The decrease in production has led to a lower allocation of emission allowances to companies. In this context, many companies have opted to sell emission allowances, pushing the price of emission allowances down.

However, EU carbon allowance prices grew to a three-month high as a European Commission official said that the EC would consider setting a price floor for carbon allowances under the EU Emissions Trading System. Current Allowance Price (per t/CO2e): €25.88.

In addition, as we enter the next trading phase (2021-2030), there will be a linear cap reduction factor of 2.2% annually applied to both stationary sources and the aviation sector.

In conclusion, a free-floating CO2 price system can be an economically efficient way to reduce carbon emissions. According to the EC, emissions of greenhouse gases from all operators covered by the EU Emissions Trading System (EU ETS) in 2019 dropped overall by 8.7% compared with 2018 levels, as a result of 9% decrease of emissions from stationary installations and a 1% increase of emissions from aviation.

Finally, it is forecast that the climate-solutions market could almost double from US$1 trillion now to >US$2 trillion by 2025 (>9% pa CAGR). Renewables, electric vehicles, batteries, biofuels, efficiency, and the circular economy will be winners longer-term.

Besides that, geo-engineering, the scale-up of climate-controlled farming, carbon capture, and mass afforestation may also emerge as part of the solution to CO2 emissions.