The year 2020 will go down in history as the year when the world turned upside down and the global economy almost collapsed. In a matter of weeks, hundreds of millions of people worldwide have lost their jobs because of mandatory quarantines.

In Africa, South America, North America, Europe and Asia – no country has been able to sustain positive growth rates or, at least, avoid the impact of this financial crisis. Even Sweden, which left much of the economy open, is now heading into its worst recession since World War II. According to Finance Minister Magdalena Andersson, the government is expecting gross domestic product to shrink by around 7% this year.

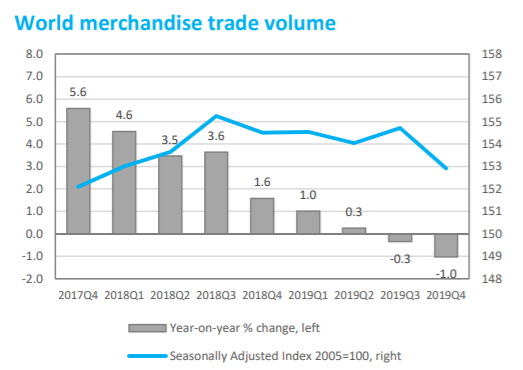

On Wednesday, the World Trade Organization said its goods trade indicator fell to the lowest level since 2011. The barometer captures the initial phases of the Covid-19 outbreak and shows no sign of the trade slump bottoming out yet. It is consistent with the WTO’s trade forecast issued in April, which projected a decline in world merchandise trade of between 13% and 32% in 2020.

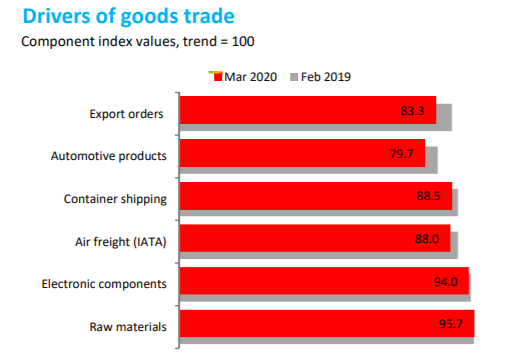

The automotive products index (79.7) was weakest of all because of collapsing car sales in major economies. The sharp decline in export orders (83.3) suggests that weak trade growth will persist in the short run. Weak demand for traded goods is also reflected by drops in indices for container shipping (88.5) and air freight (88.0).

Only the indices for electronic components (94.0) and agricultural raw materials (95.7) show signs of stability, although they remain below trend.

It is worth noting that trade was already weak in the final quarter of 2019, mainly because of trade war between major economies, especially China and the United States. In this context, the fact that tensions between those two countries are growing again suggests that problems will remain even after the pandemic crisis ends.

Once again, chips stocks have been used as a weapon in the trade war. Recently, President Donald Trump’s administration decided to cut off Huawei from accessing chips made with US software or technology.

Advanced Micro Devices is one of the American firms exposed to trade-war fallout, with roughly 26% of its revenue and 30% of its manufacturing capacity reliant on the Chinese market. On the other hand, it is a double-edged sword, as US chipmakers such as Intel are making a lot of revenue from China. Thus if China decided to respond with similar measures, North American companies would experience serious problems.

It is worth mentioning that Intel is already taking action, by investing in Chinese ProPlus, which makes EDA (electronic design automation) software, and funding Fujian-based startup Spectrum Materials. That company produces gases that are broadly used in semiconductor fabrication plants.

In addition, Trump is warning US pension funds against investing in Chinese equities. On May 12, the National Legal and Policy Center asked BlackRock to divest from the 137 Chinese companies currently listed on American stock exchanges. At least 11 have 30% or more Chinese government ownership.

The Federal Retirement Thrift Investment Board decided to pause its plans to invest in Chinese stocks this year. “At the direction of President Trump, the board is to immediately halt all steps associated with” the I Fund shift, and “to reverse its decision to invest plan assets on the basis” of the MSCI ACWI ex-US IMI index, Labor Secretary Eugene Scalia said.

Now Trump is considering requiring Chinese companies to follow the Sarbanes-Oxley Act, aka anti-fraud accounting rules. If approved, some of these companies could be forced to move to another stock exchange, as they do not allow third-party audits of their finances.

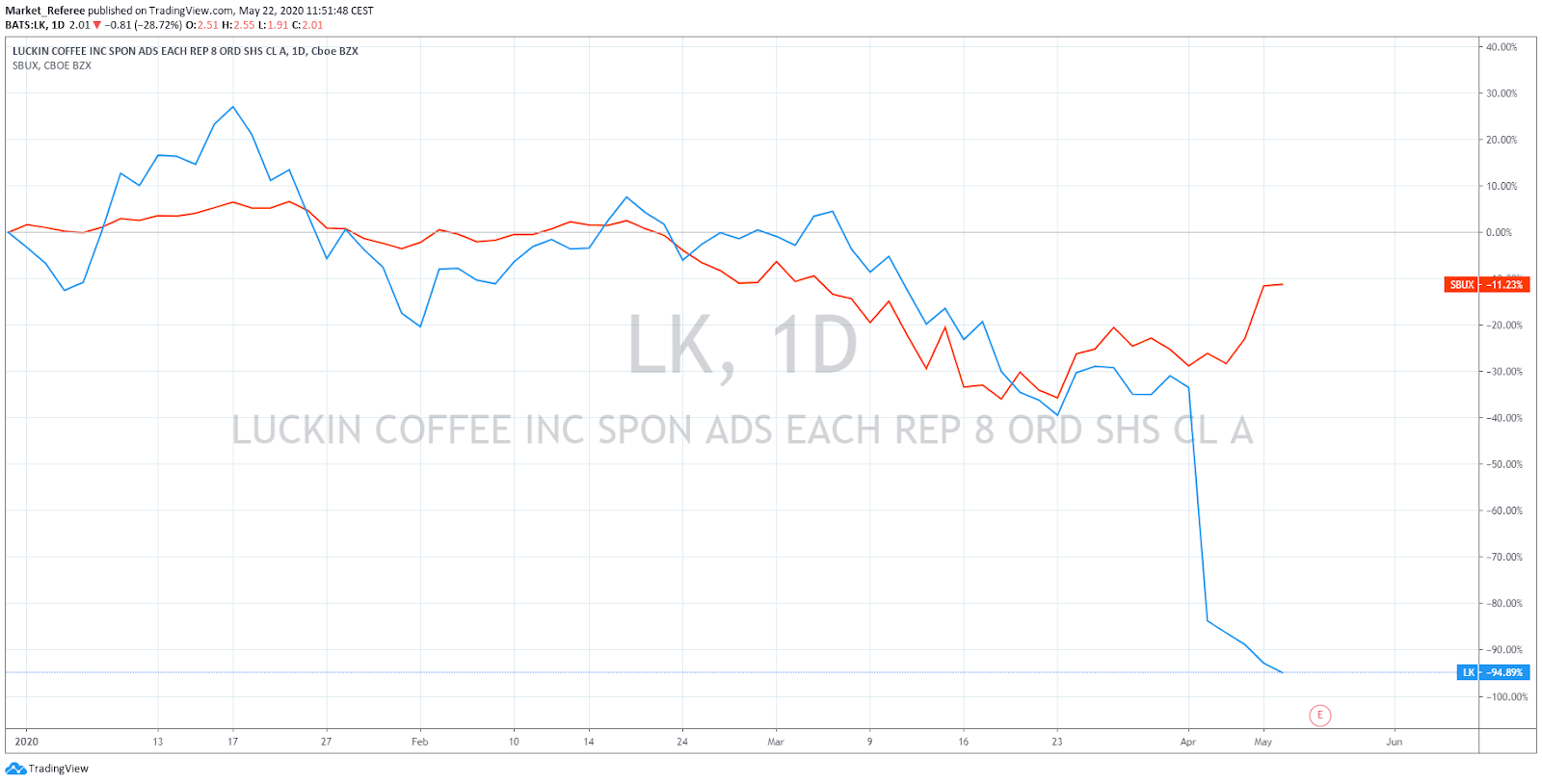

On the other hand, this requirement may save investors’ money, considering the recent Luckin’ Coffee accounting scandal. According to an internal investigation, the Starbucks rival invented more than US$310 million in sales from the second to the fourth quarter of 2019.

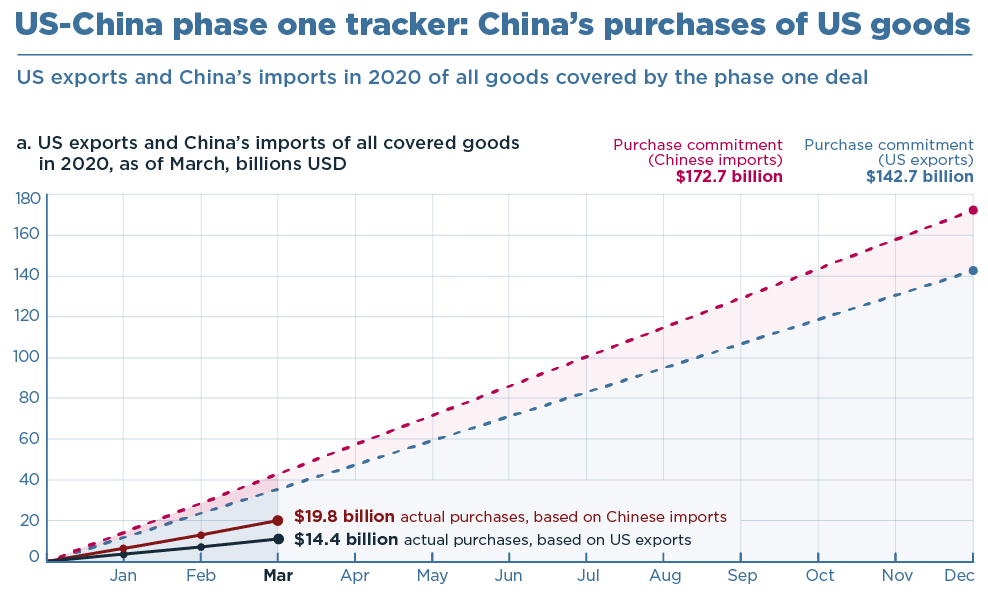

With the US elections to come in November, it is likely Trump will continue to aim belligerence at China. It is also worth mentioning that through March, China’s year-to-date total imports of covered products from the United States were $19.8 billion, compared with a prorated year-to-date target of $43.2 billion.

But it is not only China that faces challenges. According to Deloitte, more than half of the world’s countries have sought assistance from the International Monetary Fund as their currencies have depreciated sharply, thereby hurting their ability to service foreign-currency debts and risking a surge in inflation.

Besides that, declining global demand and the fall of global commodity prices have hurt emerging-country exports, also damaging debt repayment. The Group of Twenty has pledged some debt relief, and the World Bank and IMF intend to provide substantial financial resources to emerging nations.

But not every country is eager to seek debt relief, as it could harm credit ratings and future market access. According to the IMF, only 22 of 77 countries that are eligible for such debt relief have requested forbearance thus far.

Talking about the stock market, it shouldn’t be a surprise that on a year-to-date base the vast majority of indices are in the red zone. Top losers were ICAP (Indice de Capitalization Bursatil) with a 35.87% fall, IBEX 35 with a 29.98% decrease, Ibovespa with a 28.21% downfall, and DFM INDEX, losing almost 30%.

However, there were also some winners, such as the Nasdaq composite index with 3.48% growth and the OMX Copenhagen 25 index with an increase of 3.80%.

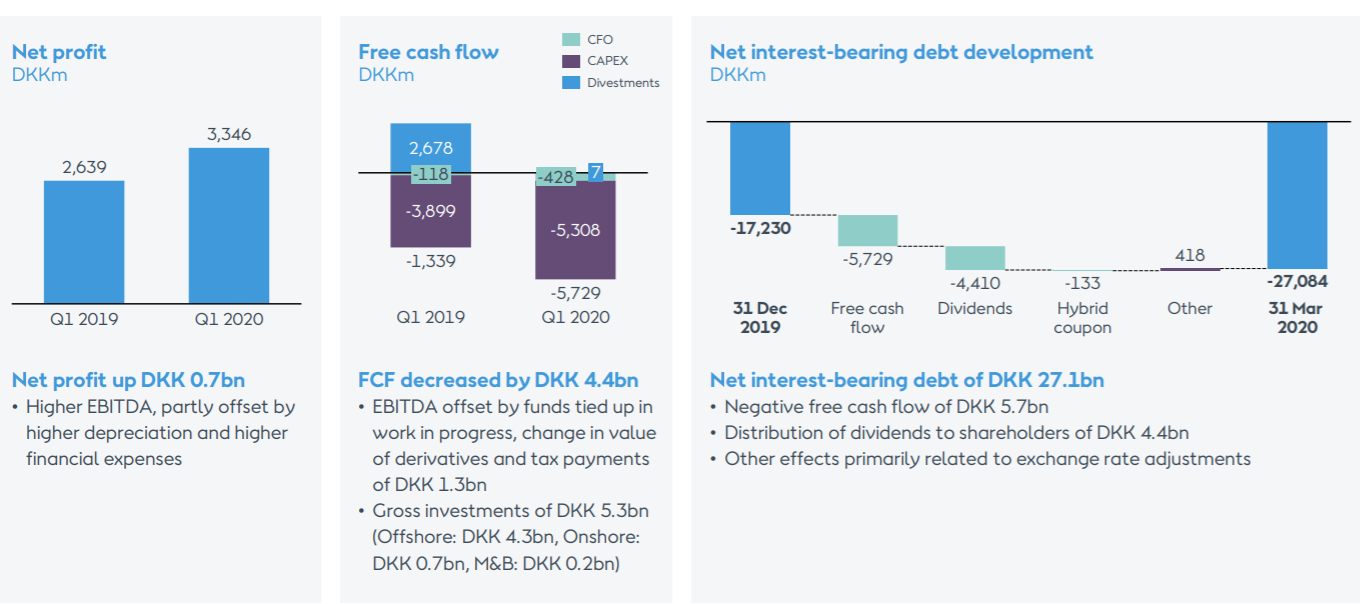

Denmark’s OMX Copenhagen 25 Index improvement can be attributed to the fact that almost half of the benchmark’s weighting comes from pharmaceutical stocks, which have proved more resilient than most in the current situation. Green stocks, such as a renewable-energy company Orsted, have also helped to boost the stock market.

The company reported strong results for the first quarter of 2020 and reaffirmed its most recent EBITDA (earnings before interest, taxes, depreciation and amortization) guidance. It doesn’t expect that the Covid-19 crisis will significantly impact its earnings this year.

Furthermore, Orsted’s EBITDA should increase in the next five years amid deployment of new wind farms and lower operating costs in the Offshore and Onshore Wind divisions. The company is benefiting from a less negative gas revaluation and positive storage hedge impacts. It is true that Orsted had higher financial charges than expected.

In the case of Nasdaq, tech stocks helped lead Wall Street higher, underlying the resilience of the technology sector to the coronavirus crisis. The Philadelphia semiconductor index, which tracks 30 chipmaker shares, is still overperforming the S&P500 index.

The iShares US Technology ETF, which seeks to track the investment results of an index composed of US equities in the technology sector, is presenting 4.30% growth this year. Finally, the First Trust Dow Jones Internet that tracks the price and yield of the Dow Jones Internet Composite Index and includes the so-called Fang stocks (Facebook, Amazon, Netflix and Google), increased more than 11% this year.

This brings us to the conclusion that investors shouldn’t put all their eggs in one basket. Diversification is the best strategy of defense against extreme circumstances like the one we are living through right now.