There is no doubt that 2020 will go down in history as one of the most unstable and volatile years. Who could have thought a couple of months ago that the US-China trade war wasn’t the worst thing that could happen to the global economy? The global spread of the coronavirus that causes the Covid-19 respiratory disease has affected almost everyone’s life in some way, especially companies in the service, wholesale and manufacturing sectors.

It is difficult to say what actually caused the outbreak of Covid-19, as both global powers accuse each other of spreading the virus. In particular, Zhao Lijian, a spokesman for China’s Ministry of Foreign Affairs (MOFA), accused the US of spreading the virus to the city of Wuhan in Hubei province, the epicenter of China’s coronavirus outbreak.

“It’s possible that the US military brought the virus to Wuhan. The US has to be transparent and make public its figures. The US owes us an explanation,” he added.

US intelligence and national-security officials, on the other hand, say the United States government is studying the possibility that the coronavirus originated in a Chinese laboratory rather than a market. Other sources told CNN that US intelligence hasn’t been able to corroborate the theory but is trying to discern whether someone was infected in the lab through an accident or poor handling of materials and may have then infected others.

These accusations do not help to lower tensions between the US and China. In fact, they may only re-escalate them.

If we look at the numbers, US manufacturing output fell 6.3% in March, the steepest drop since 1946, as measures taken to contain the spread of Covid-19 took their toll on the factory sector.

Manufacturing conditions across mainland China, in turn, stabilized in March, according to the latest Caixin PMI data. To be more precise, it rebounded nearly 10 points to 50.1 in March, up from the record low of 40.3 in February. However, it is possible that future growth in output could be limited in the coming months, as the coronavirus pandemic hits worldwide demand.

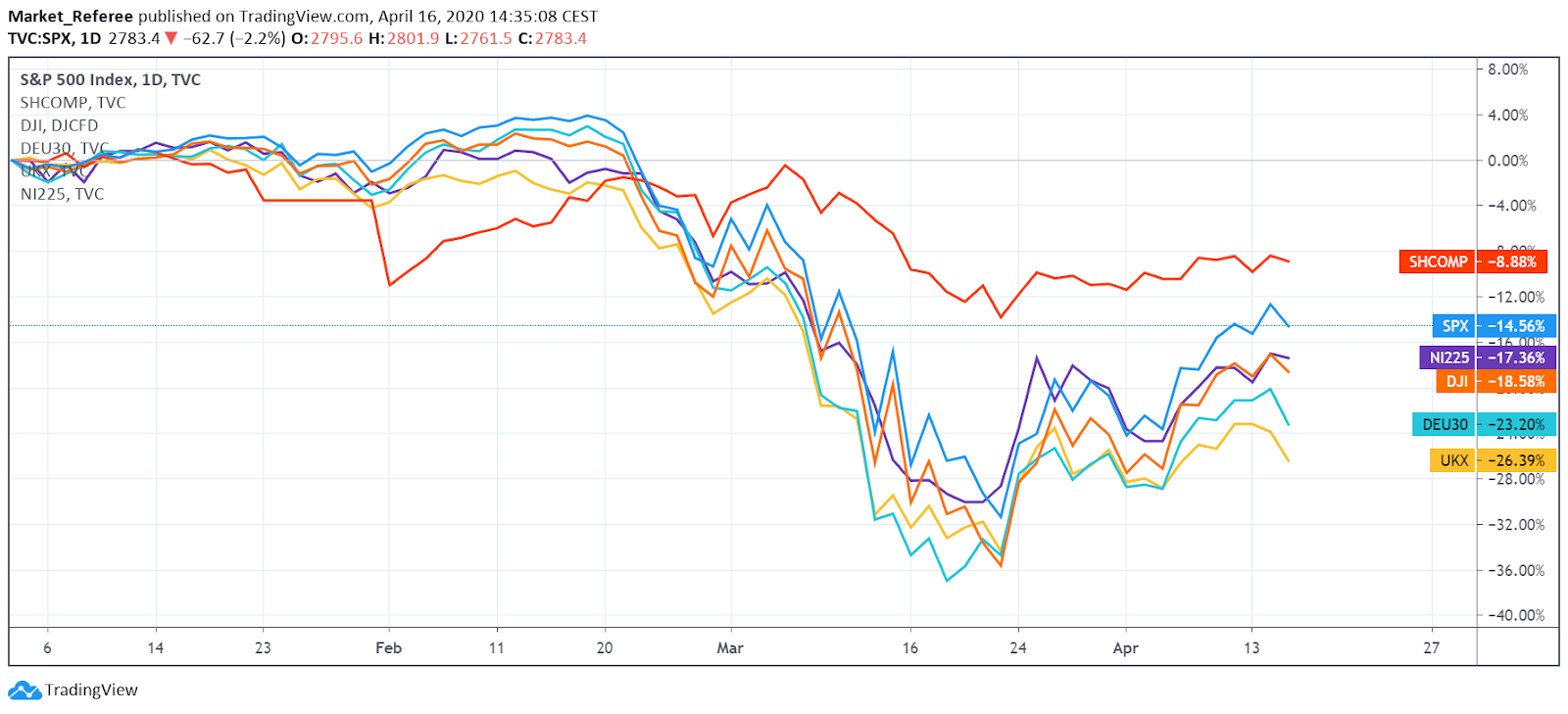

In terms of the stock markets, Chinese equity markets have also outperformed the US and most other equity markets this year. As seen in the graph below, SHCOMP fell way less than its main rivals, -8.88% vs -14.56% in case of SPX.

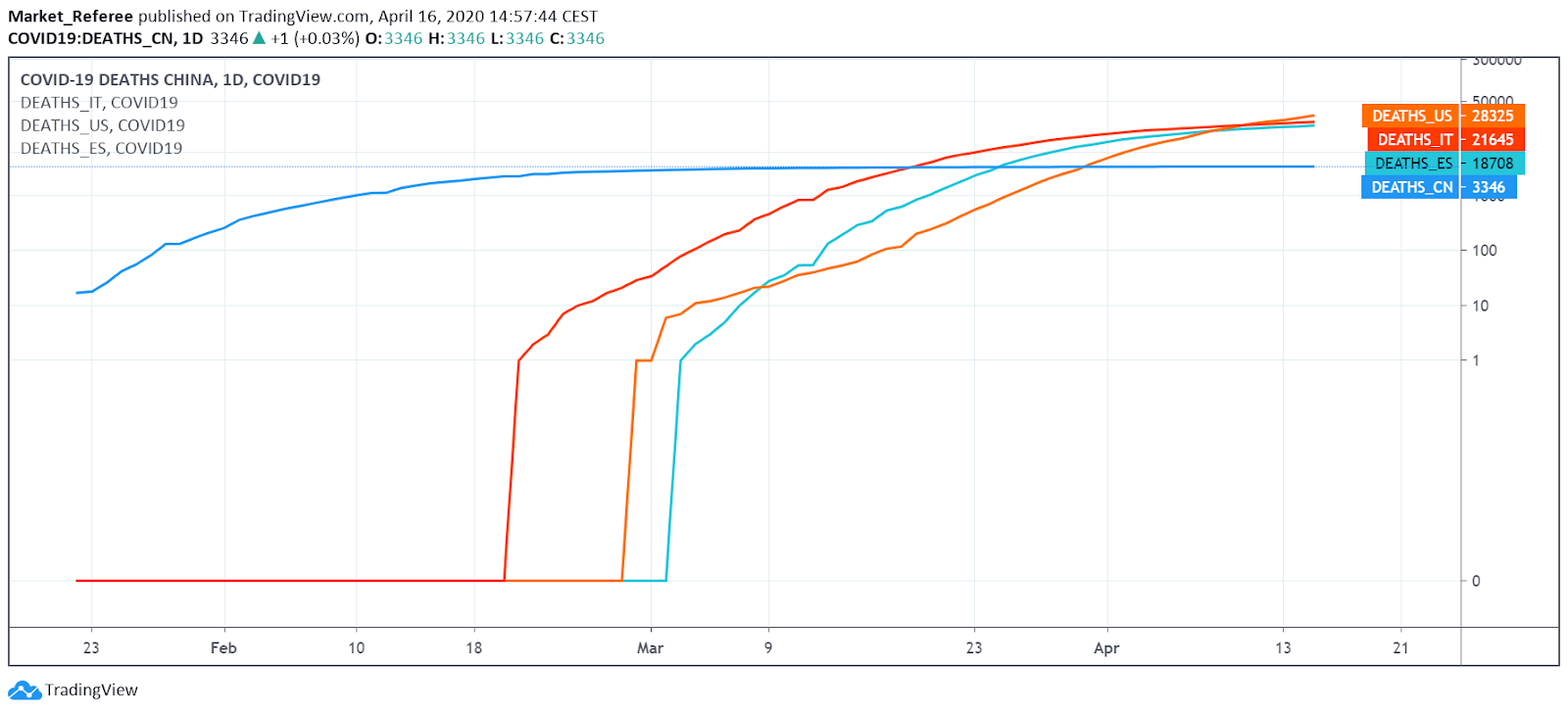

Such a difference may be attributed to one simple reason: China was able to control the virus’ spread much better and faster than some of the developed economies, including the US, Italy and Spain. The following chart illustrates this. By quickly locking down cities, shutting down business and halting public transportation to limit people’s mobility, the Chinese were able to decrease substantially the rates of decrease both deaths and new infections.

On the other hand, the Shanghai Composite Index was negative for the last decade. Over the same period, the S&P500 Index grew 147% and the Dow Jones Index +123%. The Shanghai Composite Index wasn’t even able to get back to its 2007 highs. Thus it should not a surprise that the longest bull market in US stocks led to a sharp drop in prices.

Will stimulus save economy?

Over recent weeks, the US stock markets have recovered somewhat, as the expectations of a massive stimulus package became a reality. Nevertheless, it still too early to say that the crash is over. The quarantine is still there while most businesses remain closed. The impact of Covid-19 will depend on how long the restrictions to contain the disease remain in place.

Under the assumption that the pandemic and required containment peaks in the second quarter for most countries in the world, and recedes in the second half of this year, in its April World Economic Outlook the International Monetary Fund projects global growth in 2020 to fall to -3%.

According to the IMF, growth in advanced economies is projected at -6.1% for 2020. Emerging-market and developing economies with normal growth levels well above advanced economies are also projected to have negative growth rates of -1.0% in 2020, and -2.2% if you exclude China. Income per capita is projected to shrink for more than 170 countries. Both advanced economies and emerging-market and developing economies are expected to recover partially in 2021.