From time to time, the world faces yet another obstacle to overcome. While it is true that every catastrophe is different, it is also true that most of them share similar characteristics.

For instance, if we compare the terrorist attacks on New York’s World Trade Center on September 11, 2001, with the current pandemic, we will find some similarities. In both cases, the US government closed airports, canceled or postponed thousands of flights at a direct cost to airlines, and shut down major sporting and other events, as well as restricting access to certain areas.

The only difference was the reasoning behind the decision. If in the first case, landmarks were closed primarily because of fears that they may be attacked, current quarantine measures seek to prevent the spread of a virus that can be fatal.

But where did it lead?

The week after the 9/11 attacks, the US Congress approved a law that created the Air Transportation Stabilization Board, a body authorized to provide up to $10 billion in federal loan guarantees to air carriers for which credit was not otherwise available. Nevertheless, several US airlines declared bankruptcy not long after the attacks, including US Airways and United Airlines. American Airlines laid off 7,000 employees.

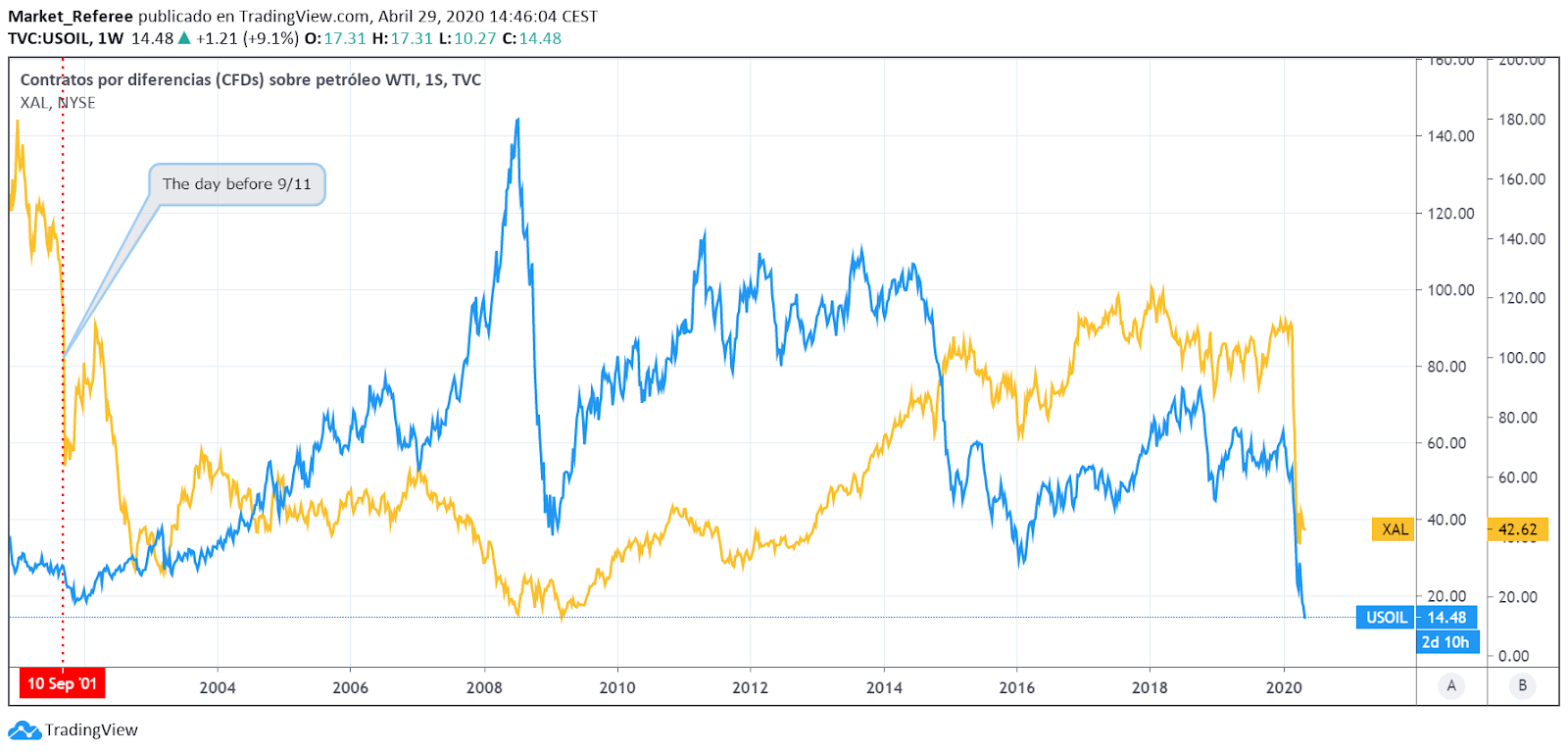

The NYSE Arca Airline Index closed on September 10, 2001, at $116.97, reopened in September 17 at $69.85, and eventually bottomed out just above $14 in March 2009. As of the market close this Wednesday, the index was at $118.12.

So it took the airline industry almost 17 years to come back to the level it had enjoyed just before 9/11. The question now is how long it will take to recover this time.

Considering the fact that lower fuel costs, an increased number of flights, air passenger growth and inflation for ticket prices have all contributed to strong profits for the industry, most probably it will be a quite challenging task, as because of the Covid-19 pandemic the recovery in demand is expected to be long and slow.

Data firm OAG has said that several years of growth has been lost by the industry and it could take until 2022 or 2023 before the volume of air passengers returns to the levels that had been expected for 2020.

US bailout for airlines

Many people expect that the pandemic will cause airline bankruptcies by the end of May unless governments and the industry take action to avoid such a situation. The Sydney-based consultancy CAPA Centre for Aviation recently warned that many airlines have probably been driven into technical bankruptcy or substantially breached debt covenants already.

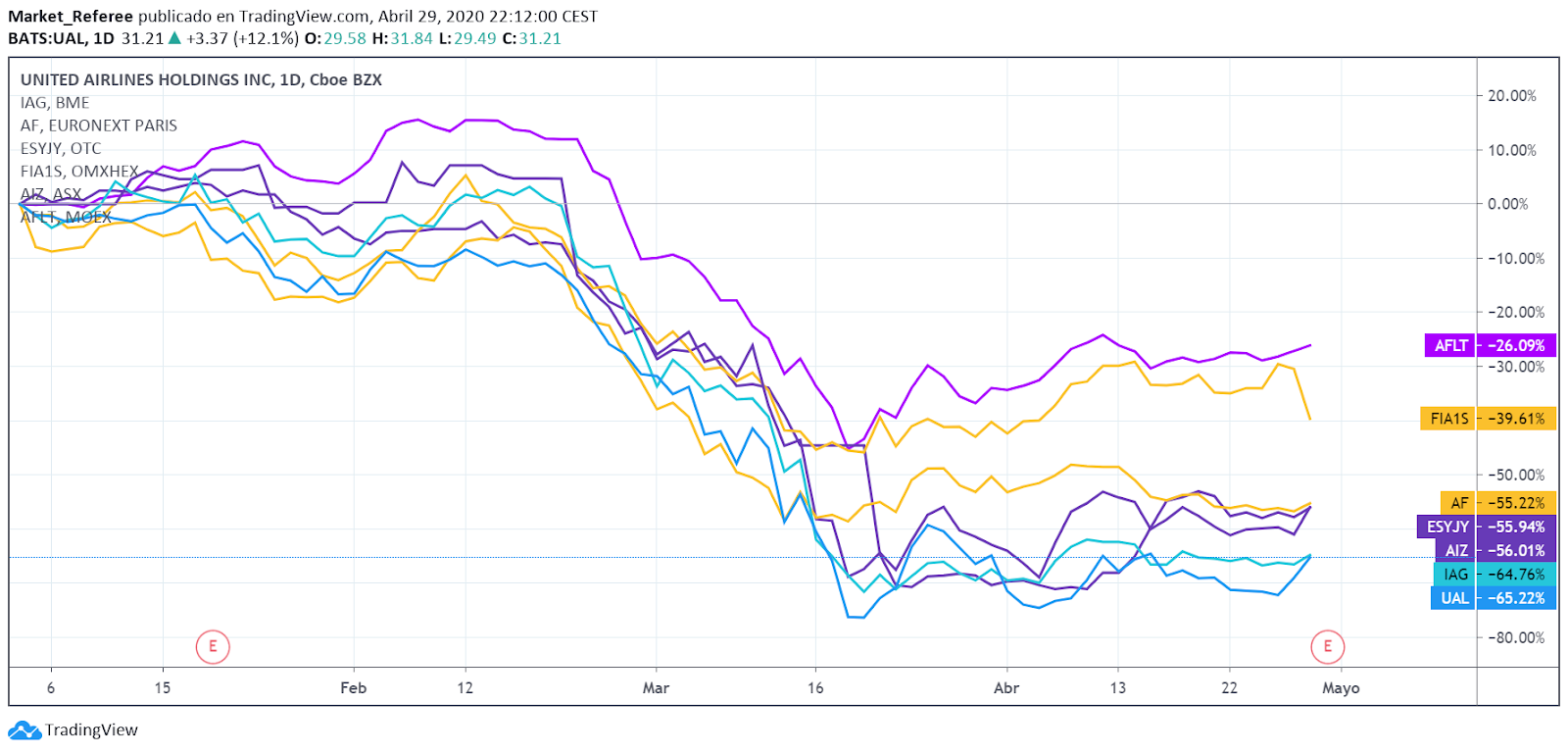

United Airlines, IAG, Air France-KLM, EasyJet, Finnair, Air New Zealand and Aeroflot have all unveiled drastic measures to cut costs in order to save their businesses. Some companies have slashed capacity, while others like Sweden’s SAS AB have temporarily laid off most staff. Flybe, Europe’s biggest regional airline, has already collapsed. Carriers could potentially lose $113 billion in revenue this year, according to the International Air Transport Association.

In this context, the US government announced a $25 billion bailout for the beleaguered airline industry. Passenger airline companies will receive direct aid as part of the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act (CARES Act) economic relief package passed last month in order to allow them to continue paying salaries and benefits to employees in the coming months.

In Europe, airlines also hope for state support. France and the Netherlands have already pledged as much as €11 billion ($11.9 billion) to save Air France-KLM. Switzerland and Austria have pledged to help Lufthansa with state-backed loans as the German airline pursues talks with Berlin over a €9 billion rescue package. Obviously, these governments have determined that they can’t allow these companies to fail.

Boeing and Airbus

Airlines are not the only ones suffering. Boeing and Airbus, two renowned airliner-manufacturing companies, also face serious problems. Deferrals of aircraft orders will cause them to reduce output for at least four years. The probability that the pandemic will have a longer effect is very high, while recovery will be slow.

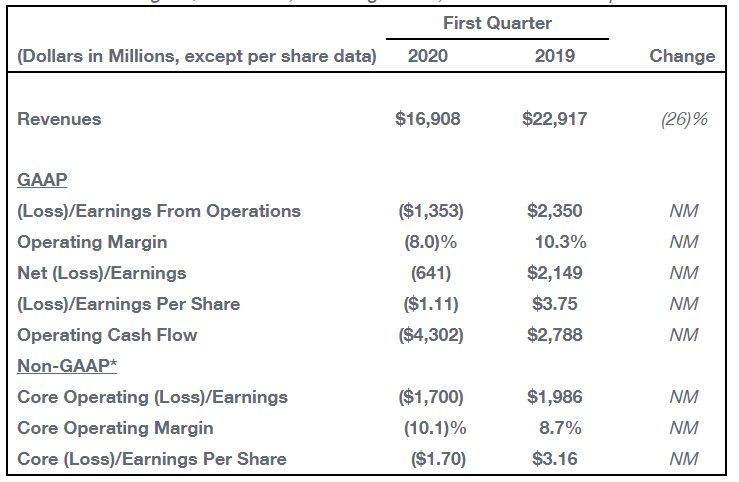

The Boeing Company reported first-quarter revenues of $16.9 billion, down 26% from $22.9 billion in the same period last year. Its operating cash flow reserves fell to negative -$4.3 billion – compared with $2.7 billion in Q1 2019 – as a result of the 737 Max grounding and the pandemic.

In addition, on Tuesday, the company’s inspections that rags and other debris were left in the fuel tanks or other interior spaces of roughly half of undelivered 737 Max jets. Boeing has lost 154 orders for the 737 this year in comparison with just 29 for the Airbus A320. Boeing could seek assistance from the Federal Reserve but not the Treasury, according to UBS.

According to The Wall Street Journal, Boeing Co faces criminal and civil scrutiny into years of widespread quality-control lapses on its 737 Max assembly line, potentially exposing the plane-maker to greater legal liability than previously anticipated by industry and government officials.

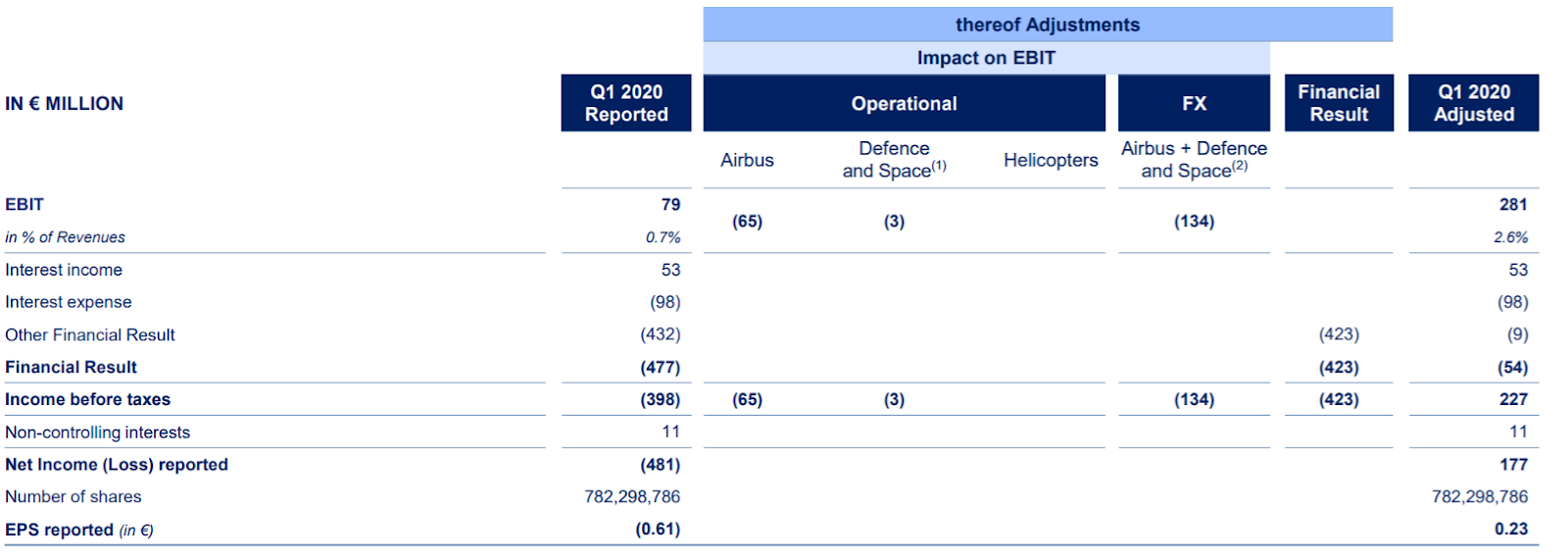

In the case of Airbus, the company has registered a first-quarter 2020 loss of €481 million, due to the aviation crisis destroying air travel demand and negating the need for new aircraft. The situation is so unclear that Airbus didn’t even give a financial outlook.

A couple of days before publishing its Q1 2020 results, the CEO of Airbus, Guillaume Faury, told employees that the company was “bleeding cash” and needed to cut costs quickly as airlines retrench. The company has already taken action, placing more than 6,000 workers in the United Kingdom and France on government-funded furlough programs.

It is important to mention that even with orders withdrawn this year, Boeing has a backlog of more than 4,000 aircraft orders and Airbus well over 6,000. Boeing 737 and Airbus A320 deliveries are expected to remain depressed for the next four years, considering the likelihood that many people won’t be willing to fly until a Covid-19 vaccine is created.

What happens post-lockdown?

As was the case with the 2001 terrorist attack, it is expected that even when the airports start reopening, passengers will be wary of air travel. Thus we still could see low demand during the initial shock period immediately following the reopening.

China’s aviation regulator said on April 22 that the daily number of transported air passenger rose 7.9% this month, as of April 21, from March, but was only at 29% of the level seen a year ago, signaling that the sector’s recovery was still fragile. The country’s number of daily flights rose only 1% in April to 6,586, amounting to just 42% of daily flights before the coronavirus struck, the Civil Aviation Administration of China (CAAC) said.

What about investors?

According to UBS’s quarterly global survey, almost half of wealthy investors expect to keep their stock portfolios at the same level in the next six months, while 37% plan to invest more. Globally, 47% of investors expect to keep their stock-market investments the same in the next six months. Additionally, 23% believe now is a good time to buy stocks, and another 61% see an opportunity to buy if stock prices fall another 5-20%.

Curiously, the UBS team came to the conclusion that the share of investors expressing short-term optimism on their region’s economy fell most in the US and least in Europe outside Switzerland.

In the case of airlines, Warren Buffett has reduced his stakes in Delta Air Lines and Southwest, selling nearly 13 million and 2.3 million shares correspondingly. Nevertheless, as mentioned above, governments may feel obligated help some of the struggling airline industry. The question now is how long it will the survived companies them to recover.