The Greek philosopher Heraclitus once said, “No man ever steps in the same river twice, for it’s not the same river and he’s not the same man.” Unfortunately, as practical experience has shown, the reality is a bit different, at least in the case of “a river of mistakes.”

Much has been said and written about the financial crisis of 2008, but this didn’t stop the world from committing the same errors. It’s no secret that credit-rating agencies played a significant role in the 2008 collapse, by giving the highest and safest “AAA” ratings to a lot of worthless mortgage-related securities.

Patricia McCoy, a Boston College scholar in financial services regulation, and Elizabeth Renuart, former associate professor at Albany Law School in New York state, have highlighted that these rating agencies are principally charged with overseeing the safety and soundness of depository institutions and not with consumer protection. However, they write, “By assigning ‘AAA’ and ‘AA’ ratings to large portions of mortgage pools, the rating agencies not only gave investors’ confidence in the safety and soundness of these investments but in many cases actually made it legally feasible for financial institutions to invest in these securities.”

Moreover, it has become apparent that there was a substantial conflict of interest: Rating agencies were paid by security issuers, not by investors in these securities. As well reflected in the 2015 movie The Big Short, actress Melissa Leo, portraying an employee of Standard & Poor’s explaining to Steve Carell’s character why S&P continued to assign “AAA” ratings to mortgage-backed securities despite knowing they were junk, said: “They’ll just go to Moody’s.”

In order to prevent this from happening again in the future, US Democratic presidential hopeful Bernie Sanders has proposed converting rating agencies into not-for-profit entities. The problem is that bond issuers pay for credit ratings and pit the agencies against one another in the pursuit of lower credit standards.

Of course, this proposal would have most probably failed. As noted by Marc Joffe of the University of Oxford, Moody’s and S&P are publicly traded companies with tens of billions of dollars in market capitalization, mostly attributable to their rating franchises. Forced conversion of these rating businesses into non-profits would have destroyed massive amounts of shareholder wealth. Stockholders might have challenged the reform as unconstitutional, triggering years of litigation.

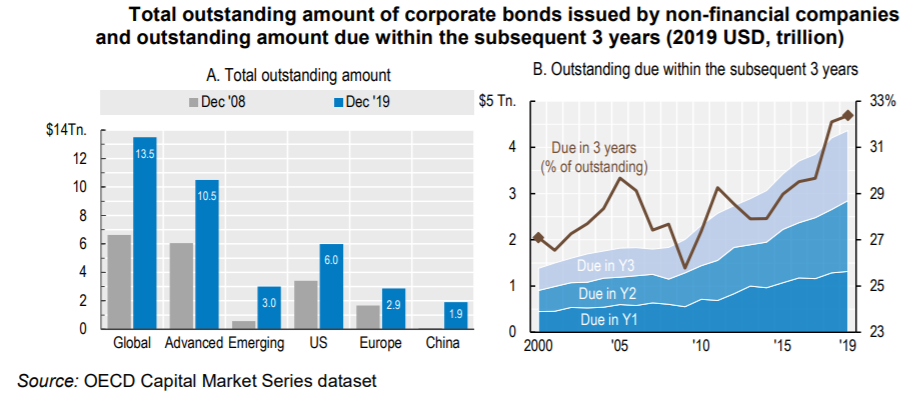

Sadly, this story is still playing out today in the US corporate bond market. Over the past four years, the US corporate bond market has increased from US$4 trillion to $5.8 trillion, reaching an all-time high in real terms of $13.5 trillion at the end of 2019. But the real problem is that the overall credit quality of corporate debt has declined, while payback requirements have increased, maturities have become longer, and investor protection has decreased. Curiously, this fall can be mainly attributed to the return of more expansionary monetary policies.

According to a report by the Organization for Economic Cooperation and Development, “Just over half (51%) of all new investment-grade bonds in 2019 were rated ‘BBB,’ the lowest investment-grade rating. During the period 2000-2007, only 39% of investment-grade issues were rated ‘BBB.’” As a result, lower-credit-quality bonds dominated the global outstanding stock. In 2019, only 30% of the global outstanding stock of non-financial corporate bonds were rated “A” or above and issued by companies based in advanced economies.

The OECD report cautioned that the portfolio allocation of all major bondholders, such as pension funds, insurance corporations and investment funds, is influenced by external credit ratings. This influence is either through regulations that use rating grades as a reference for establishing quantitative limits and capital requirements or through self-imposed rating-based investment strategies that are reflected in their investment mandates and policies.

For example, corporate bond holdings by exchange-traded funds (ETFs) that typically use passive rating-based strategies increased 13-fold from $32 billion in 2008 to $420 billion in 2018.

Interestingly also, non-financial companies have become significant owners of corporate bonds. Between 2009 and 2018, the combined value of corporate bond holdings by 25 large non-financial US companies tripled from $119 billion to $356 billion. The company with the largest portfolio alone held $124 billion in corporate debt securities. This equals the combined holdings of the world’s six largest corporate bond ETFs.

The OECD also suggests that the mechanics of the credit-rating system have allowed companies to increase their leverage ratios and still maintain a “BBB” rating.

Finally, the authors of the OECD report come to the conclusion that the significant increase of BBB-rated bonds and the declining frequency of downgrades relative to upgrades in recent years may suggest that credit-rating agencies are mindful of downgrading “BBB” issuers because of their special status just above the non-investment-grade category.

The one-year 1-notch downgrade probability is lowest for bonds rated “BBB-“, which is also the lowest rating notch before crossing the line to non-investment grade. However, extensive downgrades of BBB-rated bonds to non-investment-grade status could lead to sell-offs that put corporate bond markets in general under stress.

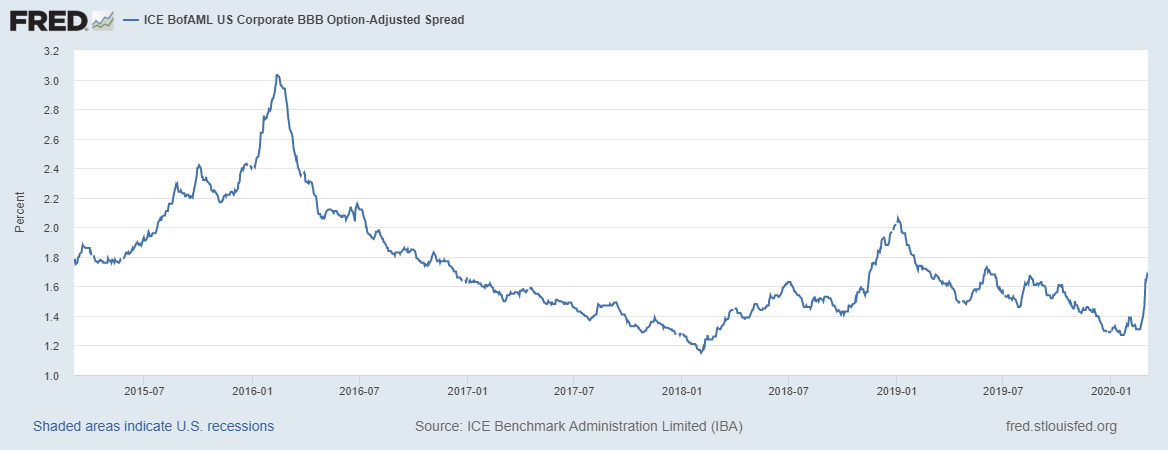

The ICE BofA US Corporate BBB Option-Adjusted Spread, which indicates the spreads between BBB-rated corporate bonds and US Treasuries, just grew, suggesting the rising risk scenario. Keep in mind that it normally happens when investors are selling bonds with a below-investment-grade credit rating and reinvest this money into the US government Treasuries. In other words, deteriorating credit conditions, measured by widening spreads, have generally been associated with slower growth, while tight spreads tend to coincide with faster growth.

Nevertheless, all this doesn’t mean that the bubble will burst the day after tomorrow. There is no evidence that the US Federal Reserve will raise interest rates any time soon, probably the opposite. However, this information may be valuable for a long-term perspective and is definitely worth checking periodically.